Nobody gets into horse racing for the paperwork—but if you’re serious about ownership, understanding the tax side will save you headaches (and money) down the stretch. Whether you’re buying your first claimer or running a full stable, here’s a practical rundown of what you need to know.

Racehorse Ownership Tax Basics (U.S.)

At the federal level, the IRS treats your racehorse operation like any other business: income gets reported, expenses get deducted (if you qualify), and the paperwork lands on your personal return. Most owners report racing activity on Schedule C (Profit or Loss From Business) or through a partnership return if you’re in a syndicate. Purse money counts as ordinary income. Deductions only apply if the IRS sees your venture as a legitimate business, not a hobby—which brings us to the next big question.

Is Your Horse Activity a Business or a Hobby? (IRS Rules)

This is the make-or-break issue. The IRS uses a nine-factor test: How do you operate? Do you have expertise or advisors? How much time do you put in? What’s your profit motive? Courts have sided with the IRS when owners showed years of losses with no real plan to turn a corner. Here’s the good news: For horses, there’s a safe harbor. If you show a profit in at least two out of seven consecutive years, the activity is presumed to be for profit—and the burden shifts to the IRS to prove otherwise. That’s more lenient than the three-of-five rule for other hobbies. Bottom line: Run it like a business. Keep separate accounts, document decisions, and have a credible path to profitability.

Entity Structure Choices: LLC vs S-Corp vs Individual Ownership

Going solo? Your racing income and expenses usually land on Schedule C. Form an LLC with partners? You’ll likely file as a partnership (Form 1065) with K-1s flowing out to each owner. An LLC that elects S-Corp status splits income into salary (subject to payroll tax) and distributions (not subject to self-employment tax)—often worth considering once net profit clears roughly $50,000 to $60,000. S-Corps add payroll and compliance overhead, so they’re not for everyone. The structure you choose affects liability, how deductions flow, and how you’re treated in an audit. Chat with a CPA who knows equine work before you lock it in.

How Partnership/Syndicate Taxes Work (K-1s Explained)

Syndicate members get a Schedule K-1 showing their share of income, losses, deductions, and credits. Unlike a simple 1099, a K-1 has multiple boxes that map to different parts of your return. Ordinary income (Box 1) is taxed at regular rates—and you may owe tax even if you didn’t receive cash, since the partnership reports allocations, not distributions. Capital gains flow through too. The key is patience: K-1s often arrive late (sometimes after March 15), which can push your filing deadline. Plan for extensions if you’re in a partnership.

Deductible Expenses: Training, Boarding, Vet, Farrier, Transport

If your activity qualifies as a business, you can deduct ordinary and necessary expenses: training fees, board, veterinary care, farrier work, and transportation. Add in employee wages (trainers, grooms, stable help), facility costs, insurance, and travel to races. The catch? You need receipts and documentation. Track names, dates, and business purpose. Mixing personal trips with race-day travel can invite scrutiny. Keep it clean and contemporaneous.

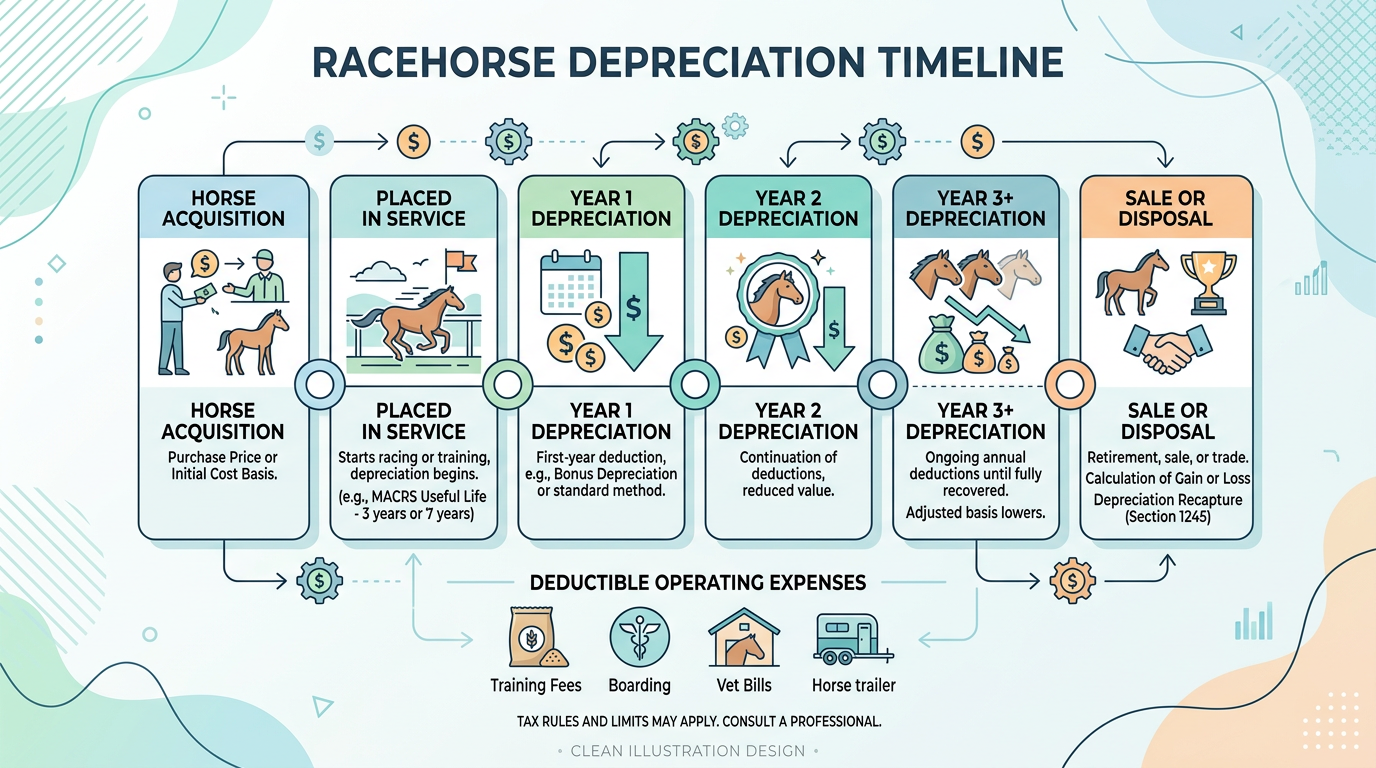

Depreciation and Amortization for Racehorses

Horses are depreciable assets under MACRS. Horses placed in service when older than two are generally 3-year property; those two or younger are 7-year property. Bonus depreciation can accelerate deductions—Congress has kept it in play for horses, and recent law makes 100% bonus depreciation permanent for qualifying property placed in service after January 2025. Timing matters: an asset is placed in service when it’s ready for its intended use (e.g., a broodmare when she’s available for breeding), not necessarily when you write the check.

When and How to Deduct Purchase Costs and Sales Expenses

Purchase price goes into your depreciable basis; you don’t deduct it all at once. Sales expenses—commission, advertising, transport to sale—reduce your amount realized and can lower gain or increase loss. Document everything: invoices, bills of sale, and proof of payment. If you sell at a loss, you don’t owe tax on the transaction, but the loss treatment (ordinary vs. capital) depends on how you held the horse and how long.

Purse Earnings, Bonuses, and Other Income: How They’re Taxed

Purse money is ordinary income, period. Report it on Schedule 1 or Schedule C. Tracks typically issue Form 1099 for purses over certain thresholds, and they may withhold (e.g., 24% if winnings exceed $5,000 and other conditions apply). Your net check is after jockey fees and other deductions—so your gross income for tax purposes may be higher than what you deposited. Report the 1099 gross, then claim the fees as separate business deductions to avoid mismatches that trigger audits.

Claiming Races, Horse Sales, and Capital Gains vs Ordinary Income

When you sell a horse, the tax treatment hinges on holding period and how it was used. Horses held for sporting (racing) and held 24 months or more can qualify under Section 1231 as livestock, potentially producing long-term capital gain. Sales under two years usually land on Form 4797 as ordinary income—and that can count toward self-employment tax. In a claiming race, the original owner keeps 100% of the purse; the claimant buys future racing rights, not past earnings. Structure and timing matter.

Breeding Income and Broodmare/Stallion Tax Considerations

Breeding changes the picture. Broodmares and stallions can qualify for bonus depreciation and special rules. Breeding stock placed in service when available for breeding gets depreciated from that point. Some arrangements use a “closing value” approach: an annual write-off based on base amount and reduction factors, with mares 12 or older sometimes written down to $1 in the year acquired. Breeding stock must typically be acquired under contract—gifts and inheritance often don’t qualify for the same treatment. Consult someone who understands breeding-specific rules.

State Tax Issues: Multi-State Racing, Withholding, and Filing Requirements

State rules vary widely. New York exempts qualifying racehorses from sales tax if purchased to race in pari-mutuel events; use tax may apply on out-of-state purchases, with caps and exemptions. California has property tax filings for racehorses. Racing in multiple states means tracking where you have nexus, what’s taxable, and whether you need to file returns or make estimated payments. Sales tax credits for tax paid elsewhere can help, but you have to document it.

International Owners and Cross-Border Tax Considerations

Non-U.S. owners racing in America face extra layers. Generally, racing for profit in the U.S. can mean being “engaged in trade or business” here—but tax treaties matter. Many treaties exempt racing income if there’s no permanent establishment. Entering a single horse in one race usually doesn’t create one; multiple races might. Form 1001 (or treaty equivalent) can reduce or eliminate withholding on purses. Without treaty relief, expect 30% withholding. Get advice from a cross-border tax pro.

Passive Activity Loss Rules and At-Risk Limitations

If you’re a passive investor (e.g., in a syndicate where you don’t materially participate), losses may be limited. Passive losses generally only offset passive income unless you dispose of the activity. The at-risk rules cap losses to the amount you have at risk—nonrecourse borrowing and certain protected arrangements don’t count. Forms 8582 and 6198 may apply. Active owners who materially participate can often avoid passive treatment, but the definitions are strict.

Recordkeeping and Audit-Proof Documentation for Owners

Document everything: horse IDs, registration numbers, acquisition dates, earnings, expenses, and the business purpose of each cost. California’s Thoroughbred Owners group flags a common mistake: Schedule C income that doesn’t match 1099s. Tracks send you a net check after deducting jockey fees and other costs. Add back track withholdings and fees to match gross, then deduct them properly. Issue 1099s to non-corporate service providers who receive $600 or more—failure can mean penalties and disallowed deductions. Keep records for at least seven years.

Year-End Tax Planning Checklist for Racehorse Owners

Before December 31: Maximize deductible expenses (vet, farrier, training) if cash flow allows. Review bonus depreciation and MACRS elections. Confirm 1099s will be issued where required. If you’re in a partnership, check estimated tax and extension timing. For international owners, confirm treaty forms are on file with tracks. And if you’re close to the two-of-seven profit test, run the numbers—strategic timing of income or expenses might help. A quick year-end review with a qualified CPA can pay off.

Owning racehorses is a thrill. Paying more tax than necessary? Not so much. Arm yourself with solid records, the right structure, and a tax pro who gets the industry—then focus on what matters: the horses. Tax forums and horse-owner communities online swap plenty of war stories; take the general wisdom, but always verify with a professional. Your situation is unique, and the IRS doesn’t grade on curve.